Weekly Update

Upcoming Events

Monday, April 15

GDPNow Update

Logan Speaks at BOJ-IMF Conference

Daly Speaks at Stanford Institute for Economic Policy Research

Tuesday, April 16

GDPNow Update

Industrial Production and Capacity Utilization Release

Jefferson Speaks at International Research Forum on Monetary Policy

Powell Speaks at Washington Forum on the Canadian Economy

Williams Speaks at Economic Club of New York

Wednesday, April 17

Beige Book Release

Bowman Speaks at Institute for International Finance Global Outlook Forum

Mester Speaks at South Franklin Circle Dialogues

Thursday, April 18

Bowman Speaks at New York Fed Regional and Community Banking Conference

Williams Speaks at Semafor World Economy Summit

Friday, April 19

Goolsbee Speaks at Society for Advancing Business Editing and Writing Annual Conference

Saturday, April 20

Blackout Period Begins

Recent News

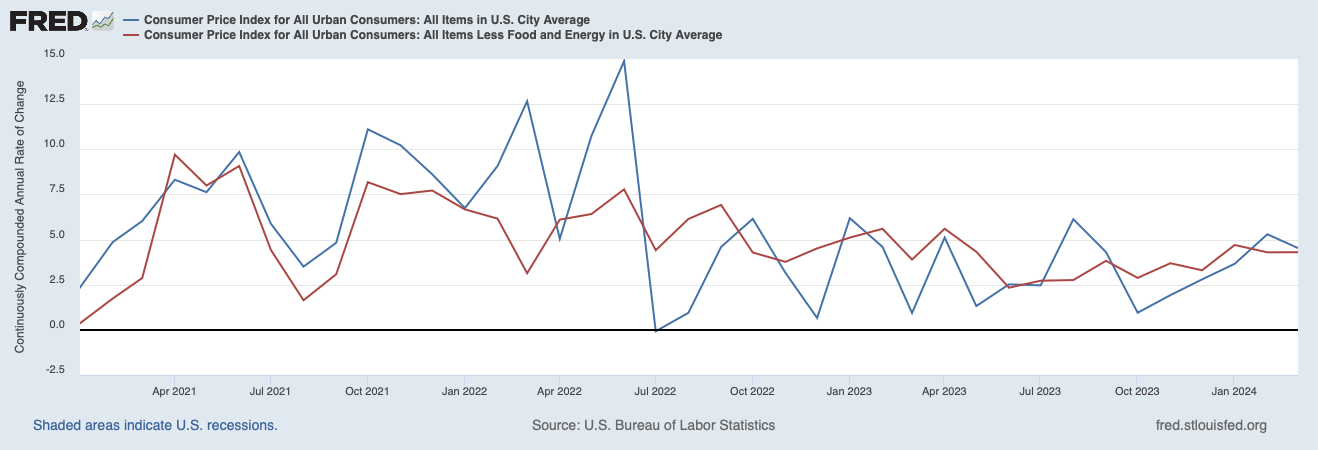

Persistent price hikes… Inflation remained high in March, according to new data from the Bureau of Labor Statistics. The Consumer Price Index (CPI) grew at a continuously compounding annual rate of 4.5 percent. It has grown at an annualized rate of 4.5 percent over the last three months and 3.2 percent over the last six months.

Core inflation, which excludes volatile food and energy prices and is thought to be a more reliable predictor of future inflation, was also high. Core CPI grew at an annualized rate of 4.3 percent in March. It has grown at an annualized rate of 4.4 percent over the last three months and 3.9 percent over the last six months.

The latest data may cause Federal Open Market Committee (FOMC) members to delay their planned rate cuts. In March, the median FOMC member projected the federal funds rate would fall to 4.6 percent this year, which is consistent with a 4.5 to 4.75 percent target rate range. One week ago, the federal funds futures market put the odds that rates would fall at least that far by the end of the year at 54.6 percent. Now, the odds are just 28.4 percent.

Market expectations of inflation are also climbing. At the start of the year, bond markets participants were pricing in around 2.17 percent inflation per year over the next five years and 2.21 percent inflation over the next ten years. Now, they are pricing in 2.47 percent and 2.39 percent, respectively.

Survey says… Inflation expectations remain elevated, according to the latest survey from the New York Fed. The median respondent continues to expect 3.0 inflation over the next year but now expects 2.9 percent inflation over the next three years, up from 2.7 percent in the prior month. The median respondent’s expectation for inflation over the five-year-horizon declined from 2.9 in February to 2.6 percent in March.

The median respondent continues to expect around 2.8 percent earnings growth. But the mean probability of finding a job in the next three months if one were to lose his or her job today declined for the third consecutive month and now sits at 51.2 percent.

Last minute details… FOMC members began discussing plans to reduce the pace of its balance sheet reduction, according to the minutes of the March meeting released last week. The FOMC had previously said it “intends to slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level it judges to be consistent with ample reserves.” However, it gave little indication as to what the level is or when it would likely reach it.

The Fed’s balance sheet climbed from $4.2 trillion in January 2020 to $8.9 trillion in May 2022. Since June 2022, the Fed has allowed up to $60 billion in Treasury securities and up to $35 billion in mortgage-backed securities to run off each month. The Fed’s balance sheet is now around $7.5 trillion.

The “vast majority” of FOMC members think “it would be prudent to begin slowing the pace of runoff fairly soon.”

Slower runoff would give the Committee more time to assess market conditions as the balance sheet continues to shrink. It would allow banks, and short-term funding markets more generally, additional time to adjust to the lower level of reserves, thus reducing the probability that money markets experience undue stress that could require an early end to runoff. Therefore, the decision to slow the pace of runoff does not mean that the balance sheet will ultimately shrink by less than it would otherwise. Rather, a slower pace of runoff would facilitate ongoing declines in securities holdings consistent with reaching ample reserves.

According to the minutes, FOMC members “generally favored reducing the monthly pace of runoff by roughly half from the recent overall pace.” Since the FOMC intends “to hold primarily Treasury securities in the longer run,” FOMC members “generally preferred to maintain the existing cap on agency MBS and adjust the redemption cap on U.S. Treasury securities to slow the pace of balance sheet runoff.”

Most FOMC members seem committed to the floor system, where reserves are “ample” and the federal funds rate is determined not by adjusting the supply of reserves but rather by adjusting the interest rate paid on reserves. Given that commitment, one might expect FOMC members to err on the side of maintaining too large of a balance sheet in order to ensure the balance sheet does not become too small to support their preferred system.