Weekly Update

Upcoming Events

Mar 27 Jefferson Speaks at Washington and Lee University

Mar 28 Barr Testifies before Senate Committee on Banking, Housing, and Urban Affairs

Mar 29 Barr Testifies before House Financial Services Committee

Mar 30 GDP Release

Mar 30 GDI Release

Mar 30 Collins Speaks at National Association of Business Economics Conference

Mar 31 PCEPI Release

Mar 31 GDPNow Update

Mar 31 Revised Surveys of Consumers Release

Mar 31 Waller Speaks at Federal Reserve Bank of San Francisco Macroeconomics and Monetary Policy Conference

Mar 31 Cook Speaks at Midwest Economics Association Meeting

Mar 31 Williams Speaks at Housatonic Community College

Recent News

Light hike… The Federal Open Market Committee (FOMC) increased its federal funds rate target range by 25 basis points at its meeting last week. The target range now stands at 4.75 to 5.00 percent.

The FOMC also revised its statement. It no longer “anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” Now, the FOMC “anticipates that some additional policy firming may be appropriate.” In the post-meeting press conference, Fed Chair Jerome Powell called attention to the words “some” and “may.”

Terminal rate… The median FOMC member continues to think the federal funds rate target will rise to 5.1 percent in 2023, the latest Summary of Economic Projections shows. That suggests the FOMC will make just one more 25 basis point hike this year.

The decision to leave the terminal rate unchanged marks an abrupt departure from the forward guidance offered earlier in the month. In his testimony before the Senate Committee on Banking, Housing and Urban Affairs on March 7, Chair Powell said “the ultimate level of interest rates is likely to be higher than previously anticipated.” Other FOMC members echoed his view at the time.

With a little help from my friends… Why did the FOMC soften its stance? In brief, its members expect to get some help tightening credit from financial markets. Chair Powell explained:

The intermeeting data on inflation and the labor market came in stronger than expected and really, before the recent events, we were clearly on track to continue with ongoing rate hikes. In fact, as of a couple of weeks ago, it looked like we'd need to raise rates over the course of the year more than we had expected at the time of the SEP in December, at the time of the December meeting. […] So, we also assess, as I mentioned, that the events of the last two weeks are likely to result in some tightening credit conditions for households and businesses and thereby weigh on demand, on the labor market, and on inflation. Such a tightening in financial conditions would work in the same direction as rate tightening. In principle, as a matter of fact, you can think of it as being the equivalent of a rate hike or perhaps more than that. Of course, it's not possible to make that assessment today with any precision whatsoever. So our decision was to move ahead with the 25 basis point hike and to change our guidance, as I mentioned, from ongoing hikes to some additional hikes maybe, some policy firming may be appropriate. So, going forward, as I mentioned, in assessing the need for further hikes, we'll be focused as always on the incoming data and the evolving outlook, and in particular on our assessment of the actual and expected effects of credit tightening.

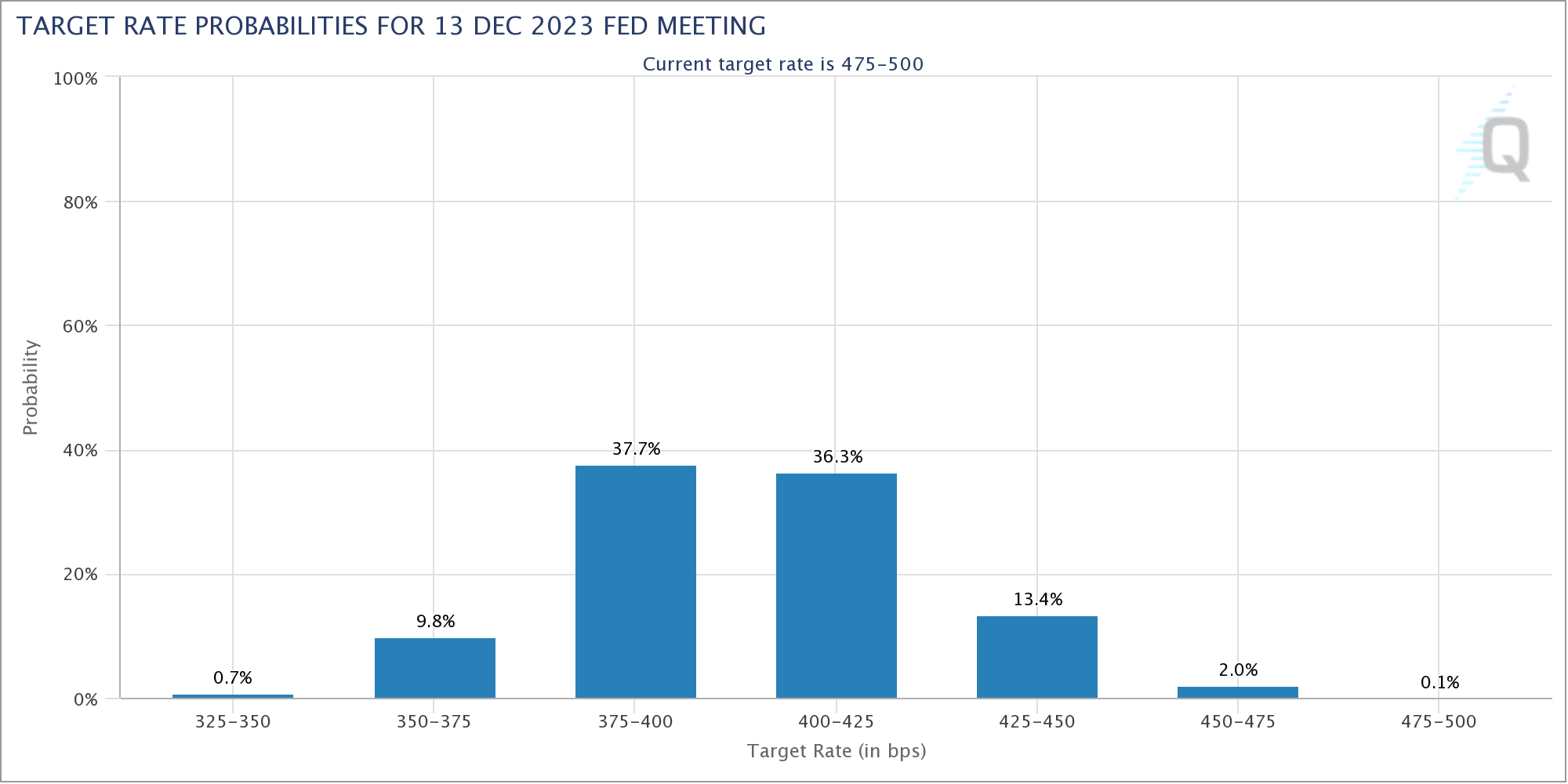

Softer still… Markets think the FOMC has already reached the terminal rate, and will begin cutting rates soon. On Sunday, the CME Group reported the odds of a 25 basis point hike in May at just 13.3 percent, while the odds that the target rate range would remain unchanged stood at 86.7 percent. There was a 10.4 percent chance that the target rate range will be 25 basis points higher than today in June; a 70.8 percent chance it will remain at 4.75 to 5.00; and a 18.8 percent chance it will be 25 basis points lower. There was just a 7.8 percent chance that the target range will still be 4.75 to 5.00 after the July meeting. There was a 68.1 percent chance that the target range will be 25 basis points lower then; a 22.3 percent chance it will be 50 basis points lower; and a 1.8 percent chance it will be 75 basis points lower.

The CME Group reported an 84.5 percent chance that rates will be at or below 4.25 percent following the December 2023 meeting on Sunday—a full percentage point below the FOMC’s implied target range projection.

Supporting role… The Fed has increased its lending to financial institutions in the aftermath of Silicon Valley Bank’s failure. According to the latest H.4.1 release, the Fed’s discount lending has increased to $110.2 billion, up from just $4.6 billion on March 8. The new Bank Term Funding Program has extended $53.7 billion in loans. The Fed also holds $180.0 billion in loans to depository institutions established by the Federal Deposit Insurance Corporation (FDIC), which are secured by collateral and guaranteed by the FDIC.

At the post-meeting press conference last week, Chair Powell said Fed officials “will continue to closely monitor conditions in the banking system and are prepared to use all of our tools as needed to keep it safe and sound.”

Looking ahead… The median FOMC member now projects the Personal Consumption Expenditure Price Index (PCEPI) will grow 3.3 percent this year, up from the 3.1 percent projection three months ago. The median inflation projection for 2024 (2.5 percent) and 2025 (2.1 percent) were unchanged from December.

Real Gross Domestic Product (GDP) is projected to grow 0.4 percent in 2023 and 1.2 percent in 2024, down from 0.5 percent and 1.6 percent, respectively, in December. The median real GDP growth projection for 2025 increased from 1.8 to 1.9 percent.

The unemployment rate is projected to reach 4.5 percent in 2023 and 4.6 percent in 2024 and 2025. In December, the median FOMC member projected a 4.6 percent unemployment rate in 2023 and 2024, and 4.5 percent unemployment in 2025. The unemployment rate was just 3.6 percent in February.

Joint statement… On Friday, the twelve regional Reserve Banks released the following statement:

The Federal Reserve Banks are committed to transparency and accountability and each Reserve Bank has existing procedures for providing information to the public. In the interest of further strengthening transparency and accountability, the 12 Reserve Banks have agreed to adopt a common policy for public requests for information and expect to implement this policy by the end of this year. Additional information on the policy will be available on each Reserve Bank’s website later this year.

The regional Reserve Banks are not subject to federal rules for information requests. Several lawmakers have expressed concerns with this arrangement, for various reasons.

Last year, then-Sen. Patrick Toomey (R-PA) claimed to have been stonewalled when seeking information on the regional Reserve Banks’ efforts to promote diversity, equity, and inclusion and the Kansas City Fed’s decisions to award and then revoke a master account for Reserve Trust. He and Sen. Warren (D-MA) introduced the Financial Regulators Transparency Act, which intended to subject regional Reserve Banks to Freedom of Information Act (FOIA) requests. The bill died with the end of the 117th Congress.

More recently, Republicans on the Senate Committee on Banking, Housing, and Urban Affairs and the House Financial Services Committee have requested information from the San Francisco Fed related to the Silicon Valley Bank failure.