Weekly Update

July 21, 2025

Upcoming Events

Tuesday, July 22

Money Stock Measures Release

Friday, July 25

GDPNow Update

Recent News

The case for cutting… In a talk hosted by the Money Marketeers of New York University last week, Federal Reserve Governor Christopher Waller explained why he believes the Federal Open Market Committee (FOMC) should reduce its federal funds rate target by 25 basis points in July.

First, tariffs are one-off increases in the price level and do not cause inflation beyond a temporary surge. Standard central banking practice is to "look through" such price-level effects as long as inflation expectations are anchored, which they are.

Second, a host of data argues that monetary policy should be close to neutral, not restrictive. Real gross domestic product (GDP) growth was likely around 1 percent in the first half of this year and is expected to remain soft for the rest of 2025, much lower than the median of FOMC participants' estimates of longer-run GDP growth. Meanwhile, the unemployment rate is 4.1 percent, near the Committee's longer-run estimate, and headline inflation is close to our target at just slightly above 2 percent if we put aside tariff effects that I believe will be temporary. Taken together, the data imply the policy rate should be around neutral, which the median of FOMC participants estimates is 3 percent, and not where we are—1.25 to 1.50 percentage points above 3 percent.

My final reason to favor a cut now is that while the labor market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed, and other data suggest that the downside risks to the labor market have increased. With inflation near target and the upside risks to inflation limited, we should not wait until the labor market deteriorates before we cut the policy rate.

Waller said the “key question for monetary policy right now is what we can discern about the underlying rate of inflation—that is, the rate excluding tariffs—based on the fundamentals of the economy.”

Federal Reserve Board staff has done work to try to estimate tariff effects on PCE prices. Using that methodology, if I subtract estimated tariff effects from the reported inflation data, I find the inflation numbers for the past few months would have been quite close to our 2 percent goal. You're not going to hear "mission accomplished" from me, but what this tells me is that underlying inflation has been lower than what is reported and close to our objective.

Waller also noted that the current federal funds rate target range is 125 to 150 basis points above the median FOMC member’s projection of the longer-run federal funds rate. That suggests monetary policy is pretty far from neutral.

While I sometimes hear the view that policy is only modestly restrictive, this is not my definition of "modestly."

In fact, the distance that must be traveled to reach a neutral policy setting weighs heavily on my judgment that the time has come to resume moving in that direction. In June, a majority of FOMC participants believed it would be appropriate to reduce our policy rate at least two times in 2025, and there are four meetings left. I also believe—and I hope the case I have made is convincing—that the risks to the economy are weighted toward cutting sooner rather than later. If the slowing of economic and employment growth were to accelerate and warrant moving toward a more neutral setting more quickly, then waiting until September or even later in the year would risk us falling behind the curve of appropriate policy. However, if we cut our target range in July and subsequent employment and inflation data point toward fewer cuts, we would have the option of holding policy steady for one or more meetings.

Alas, Waller’s case appears to be falling on deaf ears. The CME Group puts the odds of a July rate cut at just 4.7 percent.

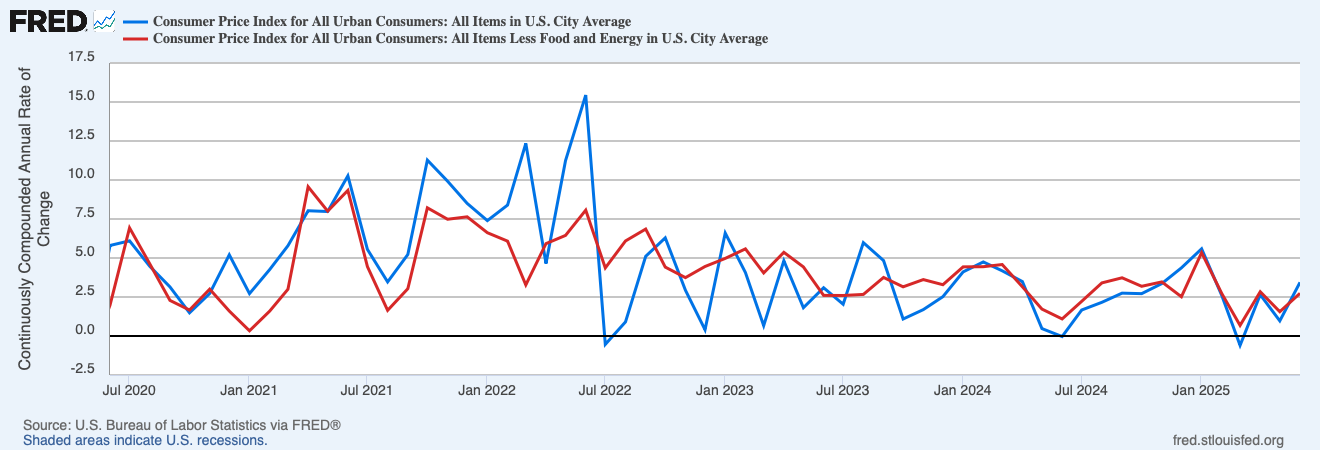

Prices… Inflation rebounded in June, according to new data from the Bureau of Labor Statistics. The Consumer Price Index grew at a continuously compounded annual rate of 3.4 percent in June 2025, up from 1.0 percent in the prior month. CPI inflation has averaged 2.4 percent over the past six months and 2.6 percent over the past twelve months.

Core inflation, which excludes volatile food and energy prices but also puts more weight on the shelter component, also increased. Core CPI grew at a continuously compounded annual rate of 2.7 percent in June 2025, up from 1.6 percent in the prior month. Core CPI inflation has averaged 2.6 percent over the past six months and 2.9 percent over the past twelve months.

Survey says… Inflation expectations have fallen for the second consecutive month, according to the New York Fed’s latest Survey of Consumer Expectations. Median year-ahead inflation expectations were 3.0 percent in June 2025, down from 3.2 percent in the prior month. Year-ahead inflation expectations peaked at 6.8 percent in June 2022, and have gradually fallen in the time since.

In June, consumers said they expected 3.0 percent inflation per year over the three-year horizon (unchanged from May 2025) and 2.6 percent inflation per year over the five-year horizon (also unchanged from May 2025).

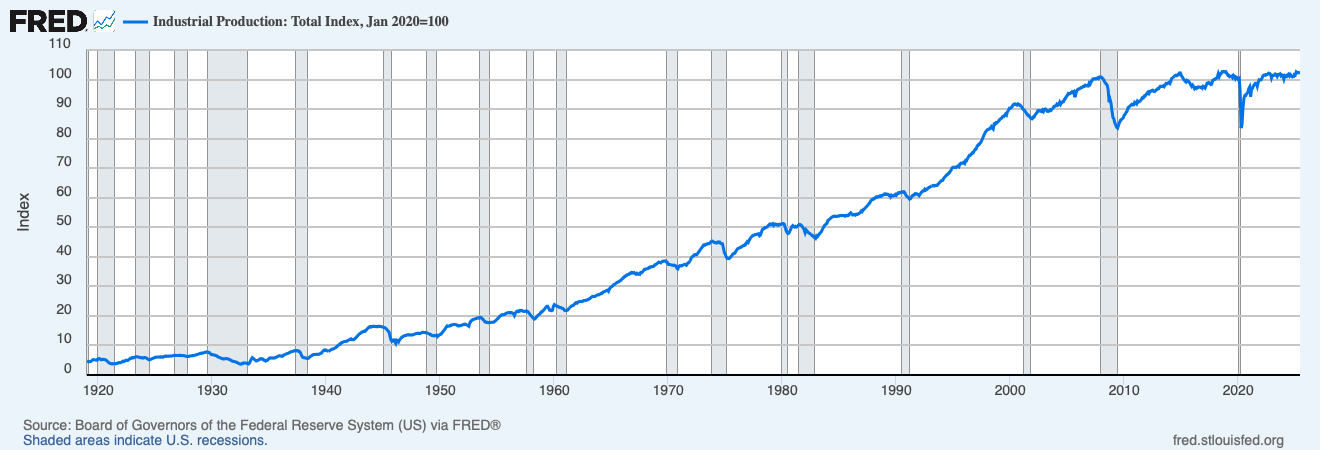

Production… Industrial production increased 0.3 percent in June 2025, new data from the Fed show. Industrial production was 2.6 percentage points higher than it was in January 2020, just prior to the pandemic. It was 0.7 percentage points higher than its year-earlier level.

Capacity utilization was 77.6 percent in June, up from 77.5 percent in the prior month. It is 1.5 percentage points above its year-earlier level and 2.0 percentage points below its long-run average.

More broadly, production appears to be rebounding. The Atlanta Fed’s GDPNow model currently estimates real Gross Domestic Product (GDP) grew at an annualized rate of 2.4 percent in 2025:Q2, after declining at an annualized rate of 0.5 percent in 2025:Q1. If the current GDPNow estimate were realized, it would amount to roughly 0.9 percent real GDP growth in 2025:H1.