Upcoming Events

Tuesday, April 22

Money Stock Measures Release

Jefferson Speaks at Philadelphia Fed’s Mobility Summit

Harker Speaks at Philadelphia Fed’s Mobility Summit

Kugler Speaks at Hurwicz Economics Institute Roundtable

Wednesday, April 23

Beige Book Release

Goolsbee Speaks at Philadelphia Fed’s Mobility Summit

Waller Speaks at St. Louis Fed Event

Thursday, April 24

GDPNow Update

Friday, April 25

Surveys of Consumers Update

Saturday, April 26

Blackout Period Begins

Recent News

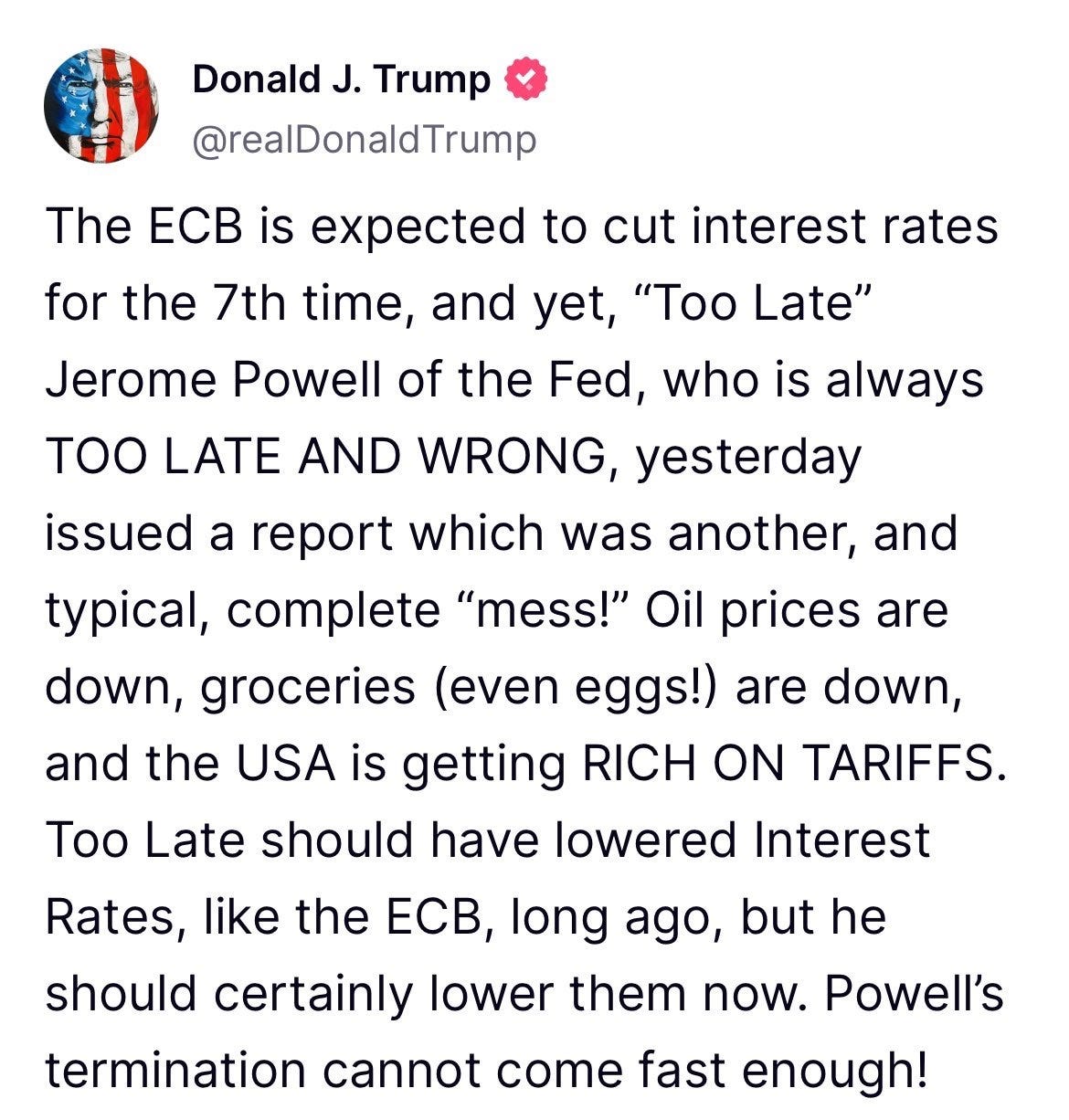

Termination day… President Trump is not happy with Federal Reserve Chair Jerome Powell. With the economy likely to slow under the weight of the administration’s tariffs and corresponding uncertainty, the president thinks the Fed should be cutting rates preemptively. Powell, in contrast, prefers a wait-and-see approach, at least partially out of fear that inflation will resurge if the Fed cuts rates too soon.

In a Truth Social post last week, the president wrote that “Powell’s termination cannot come fast enough!”

Powell’s four-year term as chair will end on May 15, 2026. Even then, he could stay on the Board as a governor until January 31, 2028. But President Trump has considered getting rid of Powell even sooner.

The Federal Reserve Act permits the president to remove a governor “for cause.” (Powell would not be able to continue to serve as chair if he were removed as a governor.) However, it is widely accepted that cause does not include mere policy disputes. That is certainly Powell’s view. When asked whether the president has the power to fire or demote the Fed chair back in November, Powell said it was “Not permitted under the law.” Just last week, he said the Fed’s “independence is a matter of law.”

President Trump disagrees. “If I want him out, he’ll be out of there real fast, believe me,” he said last week.

Earlier this year, then-Vice Chair for Supervision Michael Barr opted to step down before President Trump could attempt to fire or demote him, which seemed likely. Barr did not believe the president had the authority to do so, but did not “want to spend the next couple of years fighting about that” in court and thought “it would be a serious distraction from” the Fed’s “ability to serve our mission.”

Whether intentional or not, Barr’s decision has almost certainly improved the odds that Powell will serve out his term as chair. Since Barr was very unpopular among Republican lawmakers, President Trump would not have experienced much opposition from the home team for firing or demoting him. And, if Barr had fought the decision in court and lost, Trump could point to the precedent when dealing with Powell. By stepping down, Barr prevented such a precedent from being established.

Unlike Barr, Powell is very popular among Republican lawmakers. That puts the president in a much more difficult position. If he moves to fire or demote Powell, he will face opposition from some Republican lawmakers—and, since the decision might be overturned by the Courts anyway, it could be all cost and no benefit for the president.

Last year, now-Treasury Secretary Scott Bessent suggested Trump could appoint a “shadow Fed chair” prior to the end of Powell’s term. The shadow Fed chair would initially be appointed as a governor, with a credible commitment from the president that he or she would be elevated to chair once Powell’s term ends. The shadow Fed chair could then make speeches indicating how he or she would conduct policy in the future, which would move expectations—and markets—today.

There are at least two problems with Bessent’s suggestion, however. First, the Federal Open Market Committee conducts policy by majority vote. The Fed chair usually has an outsized voice in the process, but there is no guarantee that the remaining members of the FOMC would go along with the president’s new appointment when the time comes. The most recent Summary of Economic Projections and statements from FOMC members suggest there is broad support for Powell’s wait-and-see approach. If other FOMC members were to publicly oppose the future chair’s stated policy path, it would hamper his or her ability to move expectations as shadow chair.

Second, the president can only appoint a governor when a position becomes available. Barring a resignation or firing, the next opening will come in January 2026 when the balance of Adriana Kugler’s partial term ends. (Although she would then be eligible for reappointment, it is difficult to imagine President Trump extending the term of his predecessor’s pick.) Hence, a shadow chair would be left waiting in the wings until January—making any statements before then less credible than they would be if he or she were already on the Board.

Most likely, I suspect President Trump will reluctantly let Powell serve out his term as chair while continuing to badger and berate him from the bully pulpit.

Production… Industrial production decreased 0.3 percent in March 2025, new data from the Fed show. Industrial production was 2.5 percentage points higher than it was in January 2020, just prior to the pandemic. It is equal to its year-earlier level.

Capacity utilization was 77.8 percent in March, down from 78.2 percent in the prior month. It is 1.3 percentage points above its year-earlier level but 1.8 percentage points below its long-run average.

More broadly, production appears to be in decline. The Atlanta Fed’s GDPNow model currently estimates real Gross Domestic Product (GDP) grew at an annualized rate of -2.2 percent in 2025:Q1, after growing 2.8 percent in 2024 and 2.5 percent in 2023. The Atlanta Fed’s alternative model currently estimates real GDP grew at an annualized rate of -0.1 percent in 2025:Q1.

Meet the new boss… The Philadelphia Fed announced that Anna Paulson will serve as its next president and chief executive officer, following Patrick Harker’s retirement in June 2025. Paulson currently serves as executive vice president and director of research at the Chicago Fed.