Weekly Update

May 5, 2025

Upcoming Events

Tuesday, May 6

FOMC Meeting

GDPNow Update

Wednesday, May 7

FOMC Meeting and Press Conference

Thursday, May 8

GDPNow Update

Friday, May 9

Barr Speaks at Reykjavik Economic Conference

Williams Speaks at Reykjavik Economic Conference

Kugler Speaks at Reykjavik Economic Conference

Waller Speaks at Hoover Monetary Policy Conference

Cook Speaks at Hoover Monetary Policy Conference

Recent News

Meeting expectations… The Federal Open Market Committee is scheduled to meet this week. The Committee will likely hold its federal funds rate target range at 4.25 to 4.5 percent. The CME Group currently puts the odds of a rate cut this week at just 3.2 percent, down from 10.4 percent one week ago.

In March 2025, the median FOMC member penciled in two 25 basis points cuts this year. But markets do not expect a cut in the first half of the year. The CME group puts the odds that the federal funds rate target is below its current range following the July meeting at 80.5 percent, compared with 36.7 percent following the June meeting.

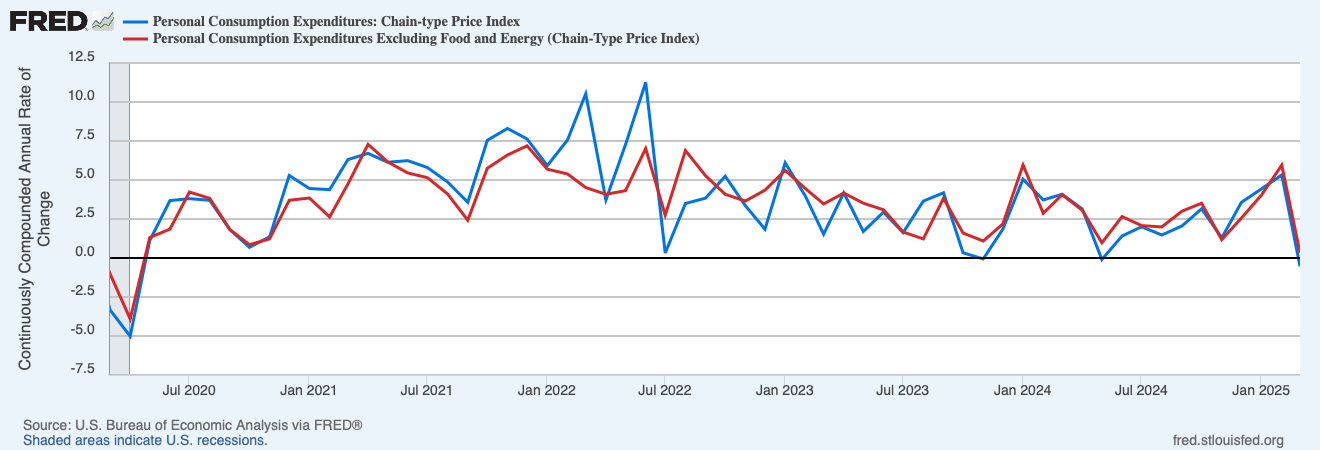

Prices… The latest data from the Bureau of Economic Analysis show that prices declined in March. The Personal Consumption Expenditures Price Index, which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annualized rate of -0.5 percent over the month. It has grown at an annualized rate of 2.9 percent over the last six months and 2.3 percent over the last year.

Core PCEPI, which excludes volatile food and energy prices, grew at a continuously compounding annualized rate of 0.3 percent in March. It has grown at an annualized rate of 2.9 percent over the last six months and 2.6 percent over the last year.

Production… Real Gross Domestic Product contracted in 2025:Q1, according to the advance estimate released by the Bureau of Economic Analysis last week. Real GDP grew at a continuously compounding annualized rate of -0.3 percent over the first three months of the year, which is the lowest growth rate recorded since 2022:Q1.

The decline in domestic production can largely be attributed to President Trump’s tariff policies. Real (inflation-adjusted) consumption and investment spending were both strong, growing 3.1 percent and 5.9 percent year-over-year, respectively. But much of that spending was directed at foreign-produced goods and services, as American households and firms attempted to avoid the tariffs that were set to take effect in early April. Real spending on imported goods was 14.5 percent higher in 2025:Q1 than it was in 2024:Q1. Real spending on imported services was 8.7 percent higher.

Are we entering a recession?

The shift from domestically-produced goods and services to foreign-produced goods and services will almost certainly be temporary. With tariffs now higher than they were in Q1, foreign-produced goods and services are less attractive. Hence, the lower-than-usual share of spending on domestically-produced goods and services in 2025:Q1 (before the higher tariffs were imposed) will be followed by a higher-than-usual share of spending on domestically-produced goods and services in 2025:Q2.

But a higher share of spending does not necessarily mean a higher level of production. The new tariffs seem likely to disrupt supply chains and at least temporarily reduce the ability of Americans to produce. If the effect is large enough, it could result in a second consecutive quarter of negative real GDP growth. If that happens, I’d call it a recession.

Fortunately, the available data supports a slightly more optimistic view at present. The Atlanta Fed’s GDPNow model currently projects 1.1 percent annualized real GDP growth in 2025:Q2. That’s slower than usual, to be sure. But I would not call it a recession.

Employment situation… The economy added 177,000 jobs in April 2025, according to the latest release from the Bureau of Labor Statistics (BLS).

Total nonfarm payroll employment was revised down by 15,000 for February 2025, from +117,000 to +102,000. It was revised down by 43,000 for March 2025, from +228,000 to +185,000.

The labor force increased from 170.6 million in March 2025 to 171.1 million in April 2025, while the total number of employed persons increased from 163.5 million to 163.9 million. The total number of unemployed persons rose from 7.1 million to 7.2 million, and the unemployment rate was unchanged at 4.2 percent.

The prime-age employment to population ratio increased. It was 80.7 percent in April 2025, up from 80.4 percent in the prior month. For comparison, around 80.6 percent of those between the ages of 25 and 54 were employed in January 2020, just prior to the pandemic.

JOLTS… The number of job openings decreased in March 2025, the BLS reported last week. There were 7.2 million openings on the last business day of the month, compared with 7.5 million in the prior month. Job openings have generally declined over the last year. There were 8.1 million job openings on the last business day of March 2024.

According to the BLS, there were 5.4 million hires in March 2025, unchanged from the prior month. There were 5.1 million separations, compared with 5.3 million in the prior month.

Within separations, there were 3.3 million quits in March 2025 (unchanged from the prior month) and 1.6 million layoffs and discharges (down from 1.8 million in the prior month).