Weekly Update

Upcoming Events

Tuesday, April 23

Money Stock Measures Release

Wednesday, April 24

GDPNow Update

Thursday, April 25

GDP Release

Friday, April 26

PCEPI Release

GDPNow Update

Recent News

Fed speak… Federal Open Market Committee (FOMC) members entered the blackout period on Saturday, ahead of next week’s meeting. Here’s what they were saying last week:

We've said at the FOMC that we'll need greater confidence that inflation is moving sustainably toward 2 percent before it would be appropriate to ease policy. You know, we took that cautious approach and sought that greater confidence so as not to overreact to the string of low inflation readings that we had in the second half of last year. The recent data have clearly not given us greater confidence and, instead, indicate that it's likely to take longer than expected to achieve that confidence. That said, we think policy is well positioned to handle the risks that we face. If higher inflation does persist, we can maintain the current level of restriction for as long as needed. At the same time, we have significant space to ease should the labor market unexpectedly weaken. Right now, given the strength of the labor market and progress on inflation so far, it's appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us.

My baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labor market will remain strong, with labor demand and supply continuing to rebalance. Of course, the outlook is still quite uncertain, and if incoming data suggest that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer.

Monetary policy is in a good place. I think we've got interest rates in a place that is moving us gradually to our goals, so I definitely don't feel urgency to cut interest rates. I think that monetary policy is doing exactly what we'd like to see. Over time, the data will inform our decisions. I think, eventually, my expectation is as inflation gets all the way to 2 percent on a sustained basis, as the economy is in good balance, interest rates will need to be lower at some point. But the timing of that's driven by the economy. The economic data, like I said, are strong on the labor market and GDP and spending. And on inflation—uh, you know—it's a little bit of a bumpy road. But, overall, the trend is—the inflation has gradually coming down.

— Pres. John Williams (New York)

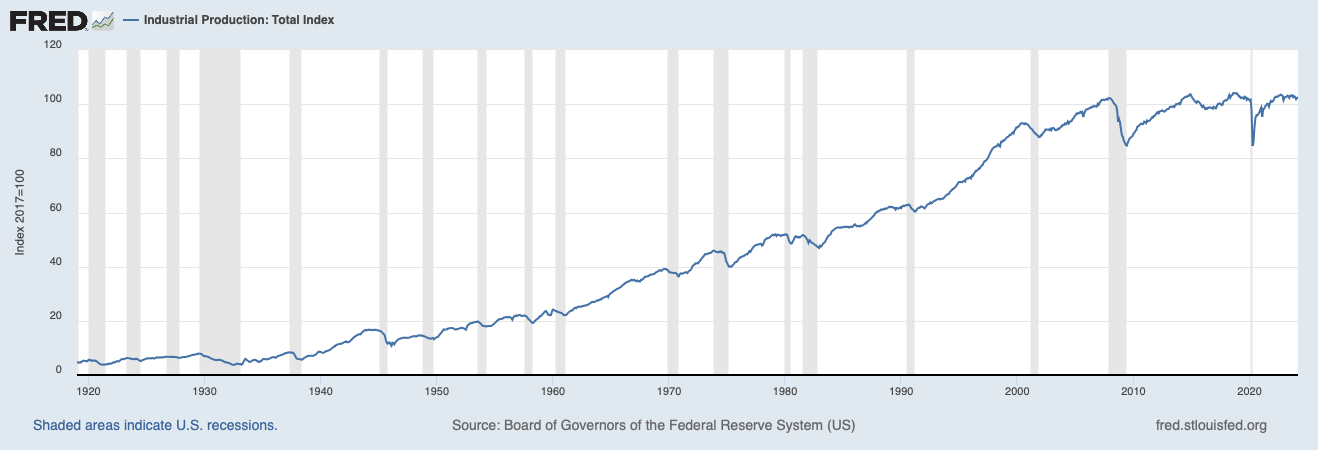

Production… Industrial production increased 0.4 percent in March 2024, new data from the Fed show. Industrial production is 1.4 percentage points higher than it was in January 2020, just prior to the pandemic. It is roughly equal to its year-earlier level.

Capacity utilization increased to 78.2 in March, up from 78.4 in the prior month. It is 1.2 percentage points below its long-run average.

More broadly, production appears to have grow at a moderate rate in the early months of 2024. The Atlanta Fed’s GDPNow model currently estimates real Gross Domestic Product grew at an annualized rate of 2.9 percent in Q1-2024. Real GDP grew 2.5 percent in 2023.