Weekly Update

Upcoming Events

Monday, March 25

Cook Speaks at Harvard University

Tuesday, March 26

Money Stock Measures Release

GDPNow Update

Wednesday, March 27

Waller Speaks at Economic Club of New York

Thursday, March 28

GDP Release

Friday, March 29

PCEPI Release

GDPNow Update

Powell Speaks at Federal Reserve Bank of San Francisco Macroeconomics and Monetary Policy Conference

Recent News

Hold on tight… The Federal Open Market Committee (FOMC) held its federal funds rate target range at 5.25 to 5.5 percent last week. At the post-meeting press conference, Federal Reserve Chair Jerome Powell reiterated that the “policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.” But he acknowledged that the economic outlook is uncertain and said the FOMC remains “highly attentive to inflation risks”.

“We are prepared to maintain the current target range for the federal funds rate for longer, if appropriate,” Powell said.

Inflation has generally slowed over the last year. The personal consumption expenditures price index (PCEPI), which is the Fed’s preferred measure of inflation, grew at a continuously compounding rate of 2.34 percent over the 12-month period ending January 2024, compared with 5.3 percent over the prior 12-month period. But it rebounded in January 2024, growing at an annualized rate of 4.1 percent.

The January uptick was widely thought to be due to insufficient seasonal adjustments. However, growth in the Consumer Price Index remained elevated in February and many now expect the PCEPI data, which will release later this week, will show that inflation remained elevated in February, as well.

Powell told reporters the FOMC was preceding cautiously:

We didn't excessively celebrate the good inflation readings we got in the last seven months of last year. We didn't take too much signal out of that. What you heard us saying was that we needed to see more. That we could, that we wanted to be careful about that decision. And we're not going to overreact as well to these two months of data, nor are we going to ignore them.

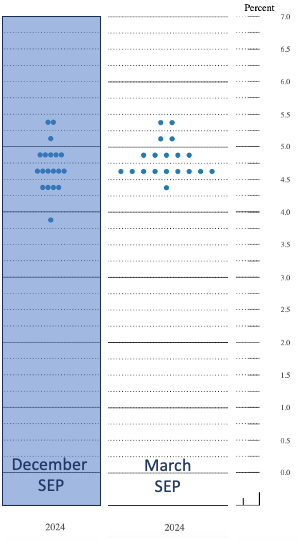

Projections… FOMC members submitted new projections last week, as described in the Summary of Economic Projections.

The biggest change in projections related to real economic activity. The median FOMC member now projects real gross domestic product (GDP) will grow 2.1 percent in 2024, up from the 1.4 percent projected in December 2023. Real GDP grew 2.5 percent in 2023.

FOMC members revised down their projection for unemployment. In December 2023, the median FOMC member projected 4.1 percent unemployment in 2024. Now, the projection is 4.0 percent. The unemployment rate was 3.9 percent in February.

FOMC members continue to project above-target inflation this year. The median FOMC member projected 2.4 percent PCEPI inflation in 2024 (unchanged from December 2023), and 2.6 percent core PCEPI inflation (up from 2.4 percent).

The headline PCEPI inflation and real GDP projections imply a sizable increase in projected nominal spending growth. Whereas the implied median nominal spending growth projected for 2024 in December 2023 was just 3.8 percent, it is now 4.5 percent. For comparison, nominal spending growth averaged 4.0 percent from 2015 to 2020.

Although there was no change in the median FOMC member’s projection for the federal funds rate this year, many FOMC members revised up their projection. In December 2023, there were five below-median projections for the federal funds rate this year. Now, there’s only one. And, whereas projections were previously as low as 3.75 to 4.0 percent, now they are between 4.25 and 5.5 percent.

Over a longer time horizon, the median FOMC member is now projecting rates will be higher than previously thought. The median FOMC member projects the midpoint of the federal funds rate target range will be 3.9 percent in 2025 and 3.1 percent in 2026, up from 3.6 and 2.9 percent, respectively. The “longer run” federal funds rate projected by the median FOMC member is now between 2.5 and 2.75 percent, 25 basis points higher than in December 2023.

Higher longer run interest rates are consistent with higher longer run:

inflation and nominal spending growth;

real GDP growth; and/or

fiscal decifits.

The median FOMC member is not projecting higher longer run inflation or real GDP growth. Correspondingly, the implied projection for longer run nominal spending growth is unchanged.

Budget issues… Last week, the Congressional Budget Office (CBO) reported that the federal budget deficit will likely grow faster than GDP over the next 30 years. The government is currently on tract to run sustained primary deficits, despite rising interest costs. The CBO projects that the deficit will reach 8.5 percent of GDP in 2054.

The CBO expects the debt-to-GDP ratio will reach a record high in 2029. But it won’t stop there: it is projected to reach 166 percent in 2054 and continue to grow thereafter. According to the report:

That mounting debt would slow economic growth, push up interest payments to foreign holders of U.S. debt, and pose significant risks to the fiscal and economic outlook; it could also cause lawmakers to feel more constrained in their policy choices.

Alas, there are no simple fixes. Restoring fiscal order will likely require significant cuts to government spending and significantly higher taxes.