Weekly Update

Upcoming Events

Monday, April 3

Cook Speaks at University of Michigan

GDPNow Update

Tuesday, April 4

Cook Speaks at Exploring Careers in Economics Webinar

Collins Speaks at Exploring Careers in Economics Webinar

Mester Speaks at Money Marketeers of New York University

JOLTS Release

Wednesday, April 5

GDPNow Update

Friday, April 7

Jobs Report Release

Recent News

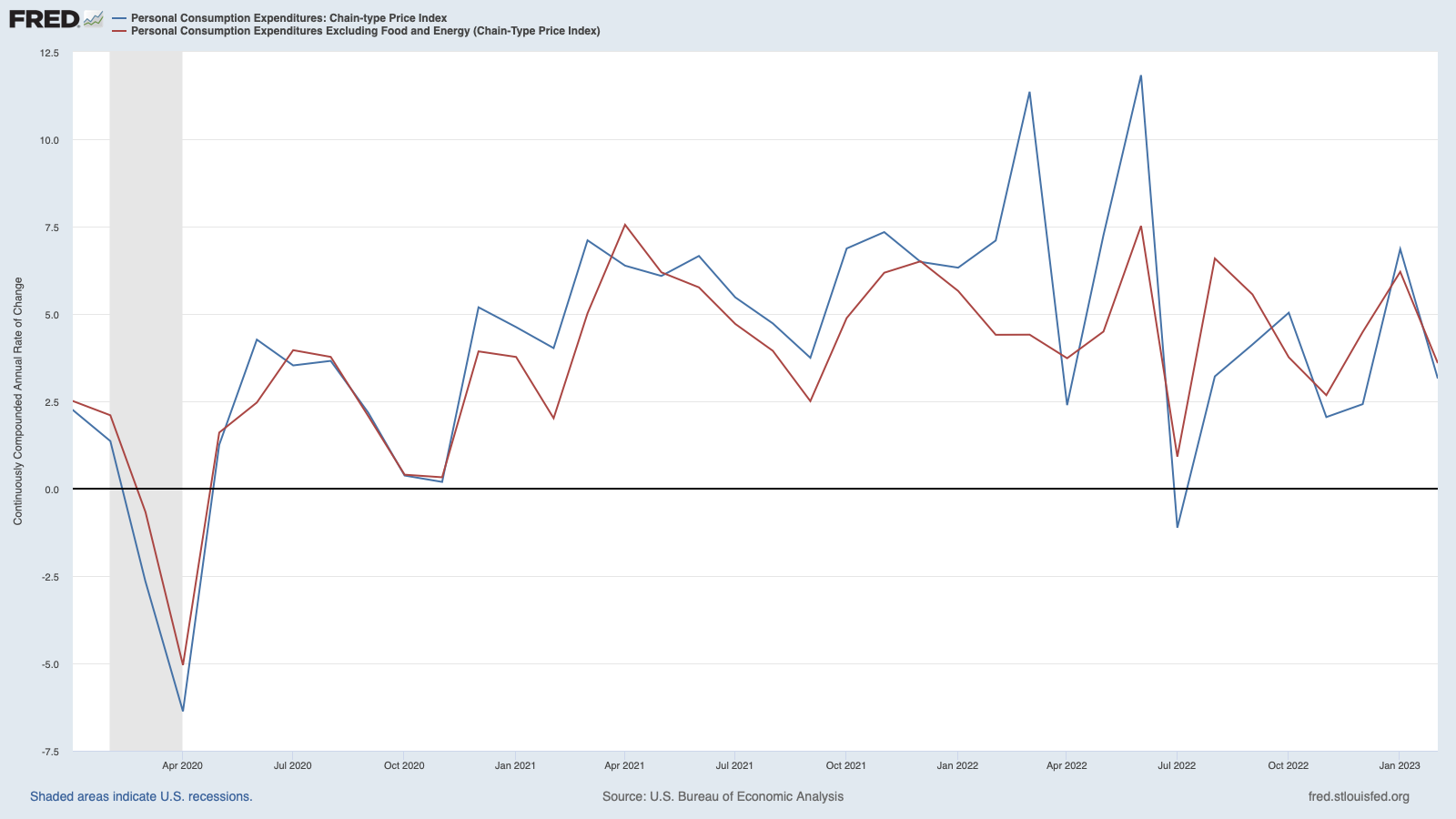

Disinflation data… On February 7, Federal Reserve Chair Jerome Powell proclaimed that “the disinflationary process, the process of getting inflation down, has begun.” The most recent data suggests he may have been right. The Personal Consumption Expenditures Price Index (PCEPI) grew at a continuously compounded annual rate of 3.2 percent in February, down from 6.9 percent in January.

Core PCEPI inflation, which excludes volatile food and energy prices and is believed to be a better predictor of future inflation rates, declined from 6.2 percent in January to 3.6 percent in February.

Of course, inflation remains well above the Fed’s 2.0 percent target. The disinflationary process has begun. But, as Powell acknowledged, “it has a long way to go.”

Market reaction… The Russell 3000 climbed 1.5 percent on Friday, closing at $2,365.47. On March 3, the Friday before the recent string of bank failures, the Russell 3000 was trading at $2352.55 .

TIPS spread… On Friday, bond markets were pricing in roughly 2.4 percent annual Consumer Price Index (CPI) inflation over the five-year horizon, and 2.3 percent over the ten-year horizon. The CPI grew 20 basis points faster on average than the PCEPI from January 2010 to January 2020. That suggests PCEPI inflation expectations over the five- and ten-year horizons are 2.2 percent and 2.1 percent, respectively.

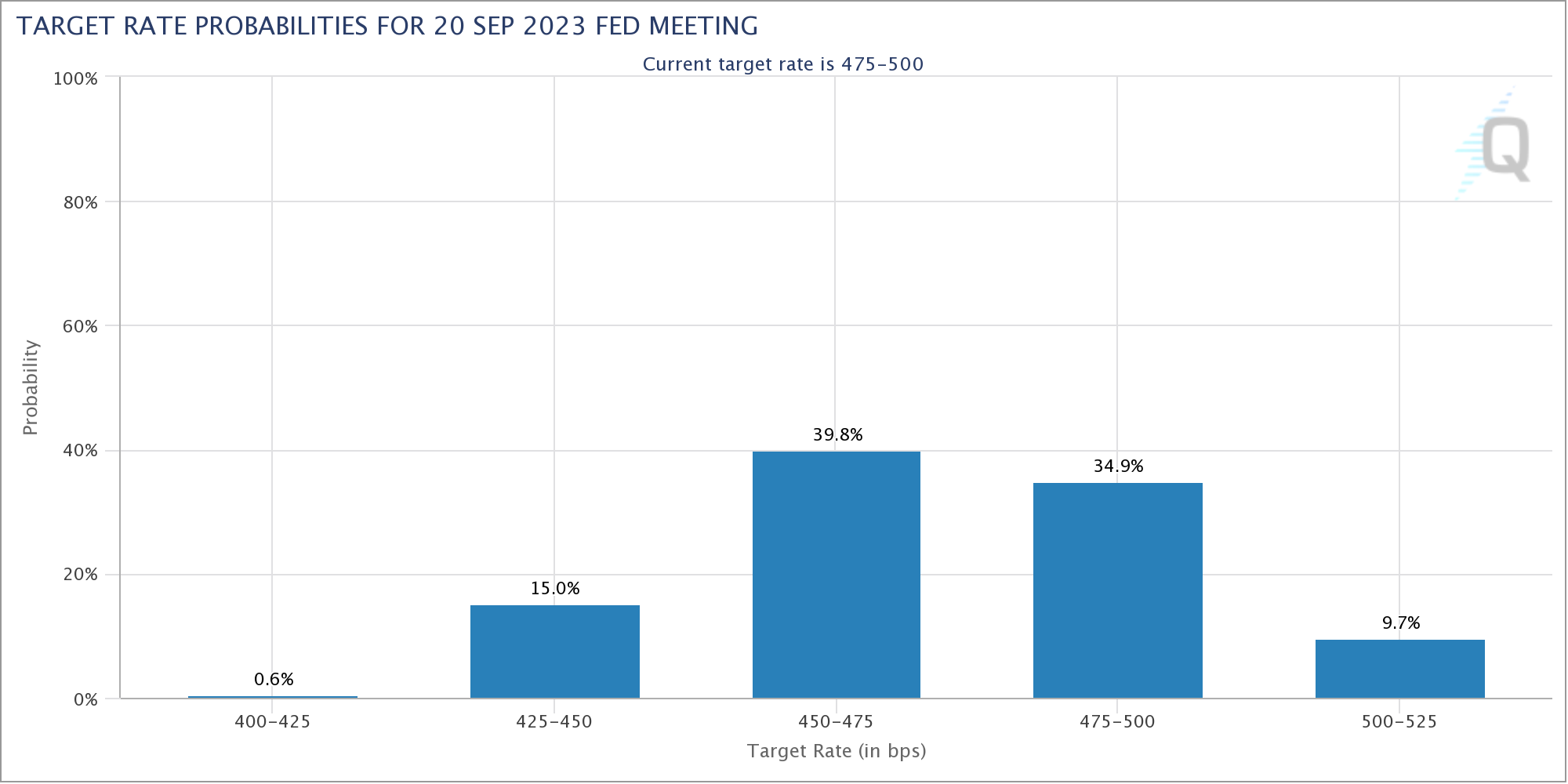

Terminal rate… Have we seen the last of the Fed’s rate hikes? The CME Group put the odds of a rate hike in May at just 48.4 percent on Sunday. Some expect the Fed will start cutting rates thereafter. The odds that the Fed’s target is lower than the current 4.75 to 5.0 percent range was 2.2 percent in June, 23.9 percent in July, and 55.4 percent in September.

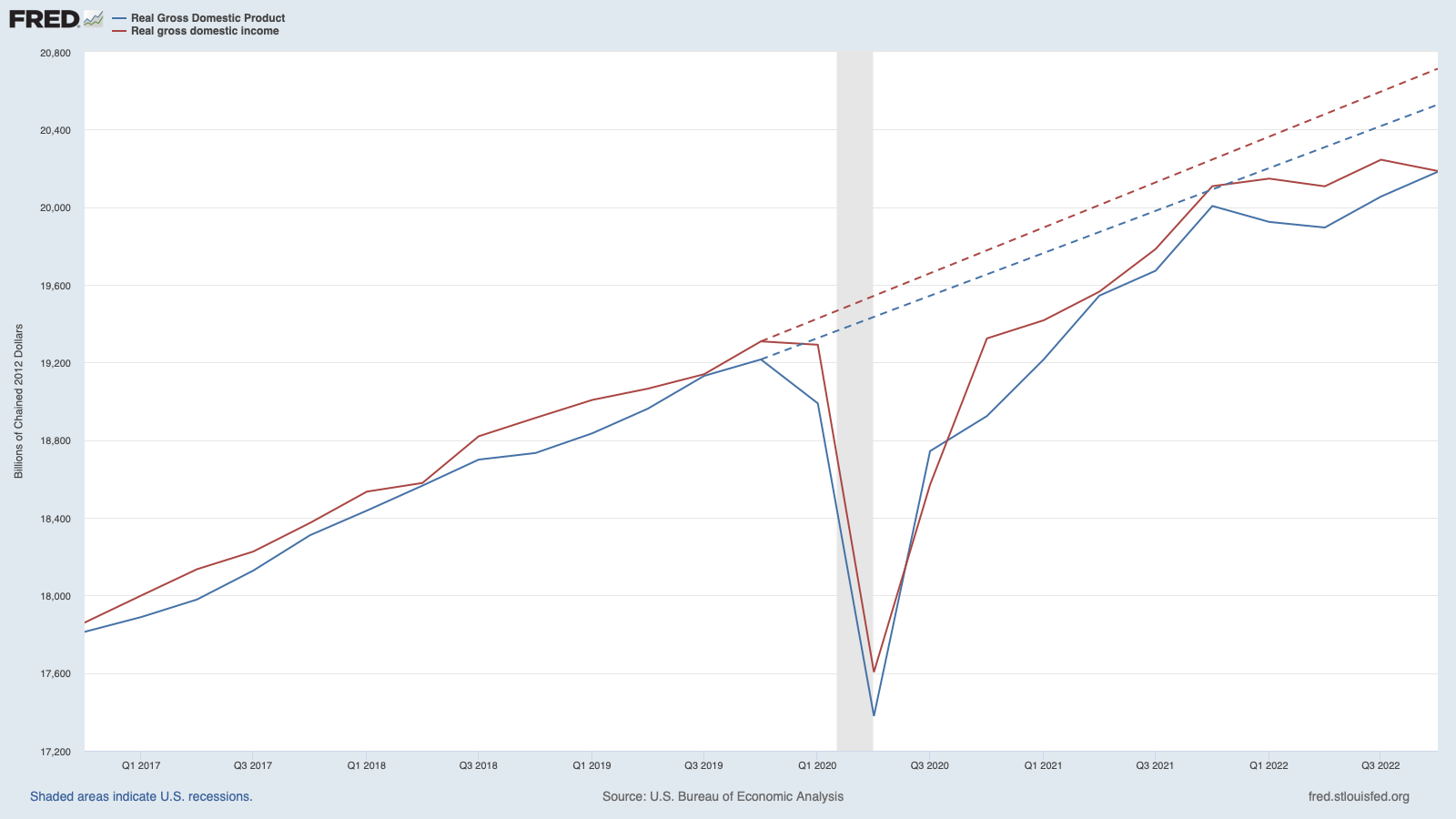

Convergence… Over the last year, pundits have debated whether Gross Domestic Product (GDP) or Gross Domestic Income (GDI) more accurately captured the state of the economy. Real GDP declined during the first two quarters of 2022. Real GDI grew slowly in Q1-2022, but only turned negative in Q2-2022. The divergence was politically useful: those who thought (or wanted to believe) we had entered a recession could point to two consecutive quarters of negative real GDP growth, while their glass-half-full interlocutors could sleep easy citing real GDI.

Now, the tables have turned. Real GDP grew at a continuously compounded annual rate of 0.8 percent over the Q4-2022, while real GDI declined 1.2 percent. The two series have more-or-less converged, which is no doubt a relief to the bean counters: GDP and GDI are essentially two sides of the same transactions.

Both measures remain below their pre-pandemic trajectories. This could indicate that there are lingering supply-side issues to be resolved; or, that there will be a small but lasting reduction in living standards following the pandemic.

Bank oversight… Vice Chair for Supervision Michael Barr testified before the Senate Committee on Banking, Housing, and Urban Affairs and the House Financial Services Committee last week on the Federal Reserve's supervisory and regulatory oversight of Silicon Valley Bank (SVB).

“SVB failed because the bank's management did not effectively manage its interest rate and liquidity risk, and the bank then suffered a devastating and unexpected run by its uninsured depositors in a period of less than 24 hours,” Barr said. He vowed to complete a “thorough and transparent” review, which will be reported to the public by May 1.

Barr said the Fed is looking at:

SVB's growth and management;

the Fed’s supervisory engagement with SVB; and

the applicable regulatory requirements.

Preliminary evidence, he said, shows “SVB had inadequate risk management and internal controls that struggled to keep pace with the growth of the bank.”

Barr offered the following timeline of interactions between the Fed and SVB:

Near the end of 2021, supervisors found deficiencies in the bank's liquidity risk management, resulting in six supervisory findings related to the bank's liquidity stress testing, contingency funding, and liquidity risk management.4 In May 2022, supervisors issued three findings related to ineffective board oversight, risk management weaknesses, and the bank's internal audit function. In the summer of 2022, supervisors lowered the bank's management rating to "fair" and rated the bank's enterprise-wide governance and controls as "deficient-1." These ratings mean that the bank was not "well managed" and was subject to growth restrictions under section 4(m) of the Bank Holding Company Act.5 In October 2022, supervisors met with the bank's senior management to express concern with the bank's interest rate risk profile and in November 2022, supervisors delivered a supervisory finding on interest rate risk management to the bank.

In mid-February 2023, staff presented to the Federal Reserve's Board of Governors on the impact of rising interest rates on some banks' financial condition and staff's approach to address issues at banks. Staff discussed the issues broadly, and highlighted SVB's interest rate and liquidity risk in particular. Staff relayed that they were actively engaged with SVB but, as it turned out, the full extent of the bank's vulnerability was not apparent until the unexpected bank run on March 9.

Tools and transmission mechanisms… Governor Philip Jefferson explained how the Fed conducts monetary policy to students at Washington and Lee University last week.

Many discussions of monetary policy simply talk about the Federal Reserve setting the federal funds rate to promote our goals of maximum employment and price stability, without giving attention to the specific actions we take to put the federal funds rate where we want it—that is, to the way we implement monetary policy. And even in economics classes that cover this topic, the teaching materials have not always caught up with the fact that we have purposely changed our implementation framework over the past decade.

Jefferson described four tools:

Setting the discount rate

Setting the interest rate on reserve balances

Setting the overnight reverse repurchase agreement rate

Open market operations

He also explained that, in an “ample-reserves environment,” the Fed’s “key tool” is the interest rate it pays on reserves balances.